At TPG, few things frustrate us more than unnecessary fees — and foreign transaction fees are near the top of the list.

You may have noticed that when you use certain credit cards abroad (or on a website not hosted in the U.S.), an additional fee is added to each purchase.

Let’s discuss what those fees are and how you can avoid them in the future.

What is a foreign transaction fee?

Foreign transaction fees are charged on certain cards when you make a purchase that goes through an overseas bank to process the transaction.

When you make a purchase while traveling or through a foreign website, banks may convert the transaction amount into U.S. dollars — often with a markup. Some credit card issuers then pass this conversion cost on to consumers as a foreign transaction fee.

Related: The best business credit cards with no foreign transaction fees

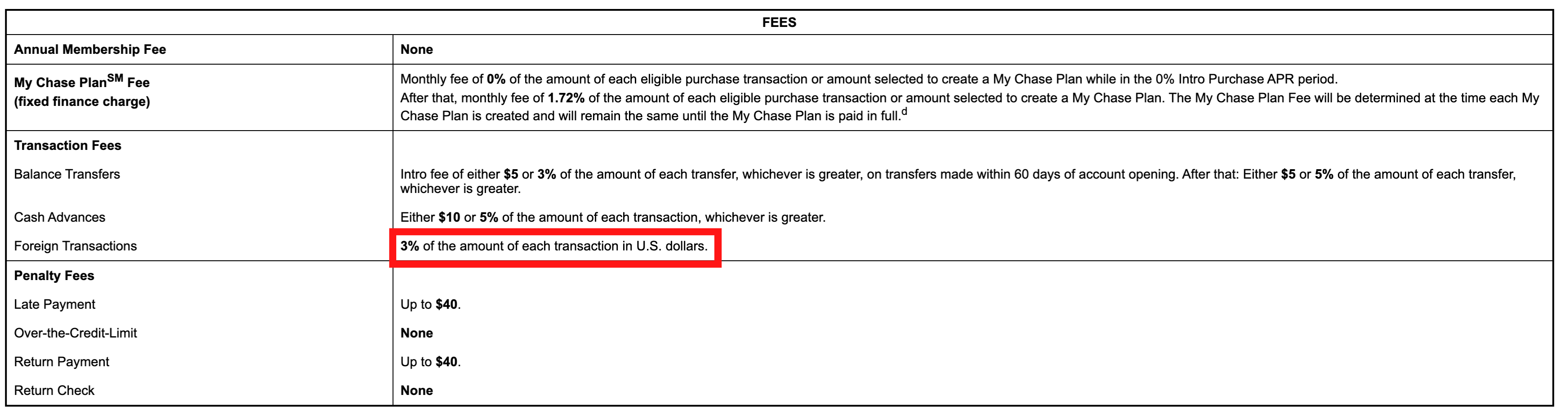

How much are foreign transaction fees?

The standard foreign transaction fee tends to be around 3%.

Visa and Mastercard typically charge a 1% processing fee and many U.S. banks tack on an additional 1%-2% fee.

However, Capital One and Discover are unique in having zero foreign transaction fees across all their credit cards.

Daily Newsletter

Reward your inbox with the TPG Daily newsletter

Join over 700,000 readers for breaking news, in-depth guides and exclusive deals from TPG’s experts

Which cards have no foreign transaction fees?

Most of the top travel rewards credit cards don’t charge foreign transaction fees. In fact, it’s rare for a card that offers travel rewards and perks to charge any foreign transaction fees. After all, it would be counterintuitive for a card marketed for travel to charge a fee on international purchases.

While some issuers charge foreign transaction fees of around 3% on some of their products, you should consider Capital One or Discover cards, since they don’t charge foreign transaction fees on any of their cards.

Card issuers are required to give potential and existing customers access to rates and fees associated with a credit card, including foreign transaction fees. Check the terms and conditions of your credit card to see whether or not your card (or the card you’re considering applying for) charges foreign transaction fees.

A rates and fees table typically lists the foreign transaction fee explicitly under a fees section.

Related: How to choose a no-foreign-transaction-fee credit card

Foreign transaction fees vs. ATM fees

Another type of fee you may hear about when you travel is a foreign ATM fee. While the two fees can apply when traveling outside the U.S., they are not the same.

A foreign ATM fee is charged when you withdraw cash from an ATM in a foreign country. Some banks waive this fee, especially if you use an ATM that falls within a specific network of banks.

Additionally, you might need to pay additional fees when you use an ATM abroad, including a flat fee from your bank for using an ATM not affiliated with the bank (typically $5), a foreign currency conversion fee (typically falls in line with foreign transaction fees at 3%) and additional fees charged by the owner of the specific ATM you use. As you can probably tell, multiple withdrawals during a trip can easily add up.

This is one reason we recommend paying with a credit card wherever possible. But in some places, cash is still king, and you’ll need to have a game plan for avoiding these types of fees — or factor them into your budget.

TPG credit card writer Danyal Ahmed recommends a Schwab Bank High Yield Investor Checking account, which offers unlimited ATM fee reimbursements for domestic and international withdrawals.

Related: Tips to save on overseas ATM withdrawals

How to avoid foreign transaction fees

Use a card with no foreign transaction fees

The easiest way to avoid foreign transaction fees is to use a card that doesn’t charge them. TPG has a regularly updated guide on the top credit cards with no foreign transaction fees that can help you choose the best cards for your trips.

However, some popular cash-back cards, such as the Chase Freedom Unlimited® (see rates and fees) and the Blue Cash Preferred® Card from American Express (see rates and fees), tend to charge foreign transaction fees.

Related: The pros and cons of cash-back credit cards

Avoid ‘dynamic currency conversion’

When using a card terminal abroad, you may be prompted to pay in the local currency or in U.S. dollars. You should always choose the local currency.

Dynamic currency conversion is a sneaky way that banks encourage you to pay in your home currency (U.S. dollars) while abroad. However, they’ll usually give you a poor conversion rate, so it’s best to pay in euros, pesos or whatever the local currency is.

Related: Dynamic currency conversion: What it is and why you should avoid it

Pay with cash

Of course, you’ll also avoid foreign transaction fees by paying with cash.

However, cash purchases will not earn you rewards, and withdrawing cash abroad may be subject to pesky fees.

Bottom line

The good news is that foreign transaction fees are much less common across top credit cards than they used to be. It seems the industry is gradually moving away from charging customers these types of fees.

Until then, check your credit card’s terms and conditions to know if you’ll be on the hook for a fee when you’re traveling — and plan your card usage accordingly.

To avoid foreign transaction fees, choose a top travel rewards card or any card from Capital One or Discover. Also, always pay in the local currency with your credit card rather than U.S. dollars to avoid poor conversion rates.

Related: How to pick the right travel credit card for you

For rates and fees of the Amex Blue Cash Preferred, click here.

{kind=link}